Scotland has recently imposed a price-floor on all alcoholic products, requiring retailers to charge at least £0.50 per unit (equal to 8g of pure alcohol, according to the UK government). The intention behind this imposition is to restrict the affordability of cheap, highly alcoholic drinks, in order to prevent overconsumption of alcohol. This is based on the argument that the availability of cheap alcohol is directly correlated with increased consumption, and thus an increase in alcohol-related death, illness, or injury.

The Scottish government believes that, in setting this minimum unit price (MUP), drinking rates amongst heavy drinkers will reduce, as it becomes more expensive and difficult to afford the quantities of alcohol needed to exceed the recommended limit of 14 units-per-week. MUP has been preferred to a simple tax increase on alcohol since “broad taxation increases do not have a targeted effect on the consumption of those most at risk (i.e. hazardous and harmful drinkers) because those that drink the most consume a disproportionate amount of cheaper products.” More expensive brands, which already impose a cost of 50p per unit or higher, will not have to alter their price to fit the new price floor.

However, the rise in cost of cheaper drinks will result in upscale brands becoming relatively cheaper, as the price differential between them becomes narrower. Demand may therefore shift towards more expensive brands as producers of cheaper brands may be unable to compete against products of better quality. This shift is also a result of the rigidity of demand for alcohol, which suggests that heavy drinkers are not particularly sensitive to changes in price. Data from the IAS suggest not only that consumers in general are fairly insensitive to price change, but that heavy drinkers are even less likely to alter their consumption in response to increases in cost. According to the IAS, a 1% increase in the cost of beer would result in no more than a 0.46% decrease in consumption amongst light to moderate drinkers, and a decrease of the demand from heavy drinkers by only 0.28%.

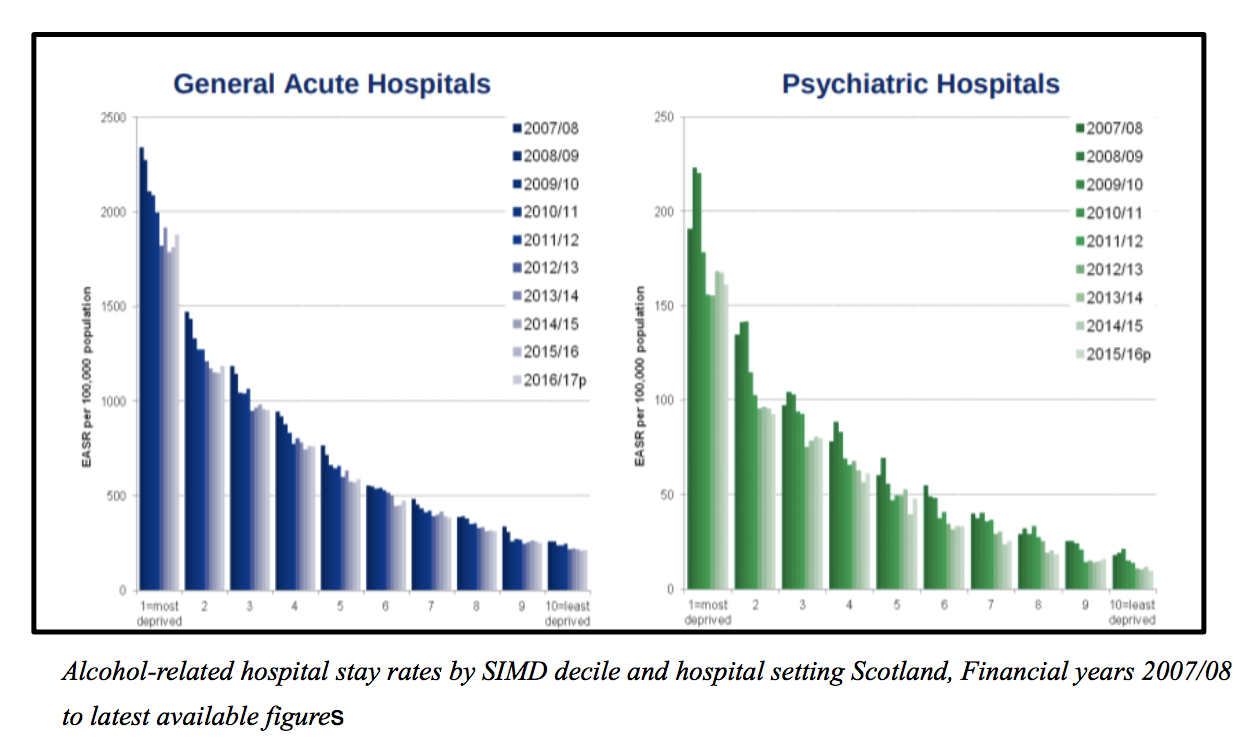

Put differently, price rigidity will prevent drinking rates from dropping. Rather, this strategy is more likely to result in a much higher cost burden on a social group characterised by low incomes and tight budgets. As the graphs below (retrieved from an ISD Scotland Report) demonstrates, the vast majority of discharges from both acute and psychiatric care with an alcohol-related diagnosis come from the most deprived areas of Scotland, and shows a clear positive trend between socioeconomic status and rates of discharge.

Moreover, private importations or smuggling of alcohol from other parts of the UK would provide heavy drinkers with a different channel through which to obtain alcohol. Profits of legitimate retailers (such as supermarkets and corner shops) are also likely to lose out on profits which will be transferred to those smuggling from England, as well as to English retailers close to the Scottish border, which may benefit from private importers travelling solely with the intention of purchasing alcohol.

This kind of behaviour in response to high alcohol prices has already been observed in similar scenarios, perhaps most notably in Scandinavia. In Sweden, for instance, it is only possible to buy any alcoholic drink above 3.5% at a state-owned store at a heavily inflated price (a result of high alcohol taxes). According to a 2010 research paper by Nina-Katri Gustafsson, Swedes living closer to Denmark and Germany purchase almost half of their alcohol in either country as a result of the lower costs,.

Many Danes behave similarly and bring in cheaper drinks from neighbouring Germany. Not surprisingly, a 2009 research paper by Ulrike Grittner and Kim Bloomfield showed that the amount of alcohol imported decreased after the Danish government reduced taxes in 2003, and that the Danish reduction of taxation on alcohol led to no increase in consumption in southern Sweden, nor amongst the Danish consumers themselves.

Four conclusions follow. First, increasing the price of alcohol is unlikely to affect consumption rates significantly. Second, Scotland’s MUP is more likely to impose a larger cost burden on poor consumers. Third, price differences in neighbouring markets are likely to lead to private importation and arbitrage. In the Scottish case, we can expect much of this to occur amongst Scots living close to the English border. Finally, the MUP is unlikely to bring significant benefits to the NHS budget. One may welcome efforts to contain the costs suffered by the NHS in dealing with heavy drinkers, such as ambulance or police callouts, and the need for hospital treatment. While the current tax revenues from alcohol duties in Scotland amount to around £1 billion, the annual cost of alcohol on the NHS stands at around £3.6 billion.

Evidently, there is an injustice in taxpayers subsidising heavy drinkers to the tune of £2.6 billion. Rather than raising taxes to fill this gap, however, drinkers could be dissuaded from overconsumption by charging them when they access the NHS as a consequence of a drinking problem. Rather than forcing poorer drinkers to tighten their budgets even further with an MUP, a restriction on free NHS access would target only those who drink to extreme levels, and would end the unjust carrying of hazardous drinkers by ordinary taxpayers.