The Greeks have voted and the left-wing Syriza emerged as the clear winner. There will now follow intensive discussions about Greek reforms and the relationship between Greece and the rest of the world. The labour market is one of the core battlegrounds in Greece. It is very difficult for the country’s unemployed to re-enter the labor market. This is borne out not only by the high unemployment rates but also by data on duration of holding current job. In no Eurozone country has the average employed worker held his or her job as long as in Greece. It is not clear whether the new government has either the incentive and/or the means to adjust the privileges of labour market insiders for the benefit of current outsiders.

High unemployment and long job duration

Greek unemployment stood at 26.2% in the 3rd quarter of 2014. Among the under-25-year-old, the rate is even 50.1%. The new government will be judged also on what it does to these figures.

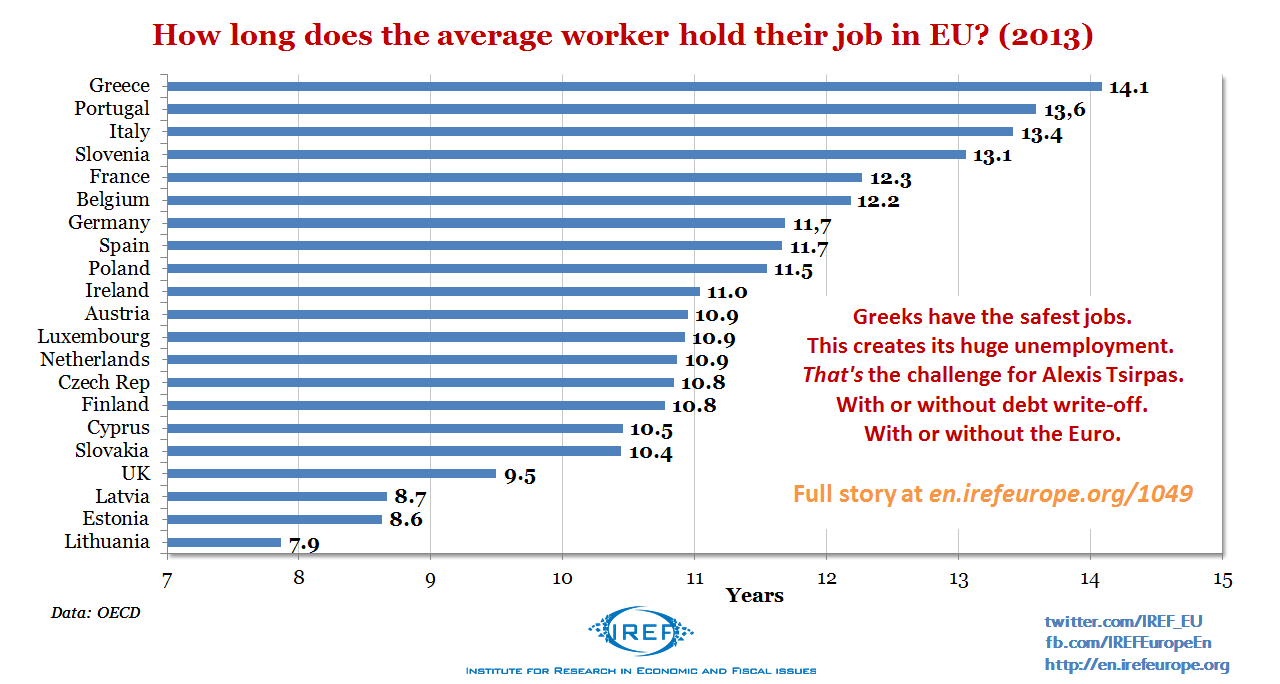

Another indicator of the stuffy conditions on the Greek labour market is the length of time for which those employed have held their current job. At a first glance, a long time on a job may seem like a good thing, providing workers with job security. That consideration, however, leaves out the unemployed. An all-society perspective, therefore, reaches a different verdict. Average duration of current job is also an “inverse” indicator of the frequency of changing job. The greater the duration, the less frequent are job changes, and the less frequently has an unemployed person a chance to get a job.

The average Greek was in 2013 in their job longer than any other average Eurozone worker: 14.1 years, according to OECD data. There were two other countries with high duration, 13.6 years in Portugal and 13.4 years in Italy. In Germany (11.3) or in the Netherlands (10.9) the duration is much lower and in the Baltic states of Lithuania, Latvia and Estonia it is considerably lower (8.4 years on average).

Outsiders vs. Insiders and downward rigidity of nominal wages

Nominal wages (i.e. the current amount of local currency the worker is paid) are often rigid downwards. That is to say, no matter what happens to labour supply or demand, nominal wages do not fall, or fall only minimally. A number of factors contribute to this, including minimum wages, unfair dismissal rules and the collective bargaining binding in many occupations. And it is these very factors which also contribute to lengthening of stay in a given job. When employers demand less work and nominal wages cannot adjust, quantity adjusts instead. Instead of there being a similar number of jobs albeit for a lower wage, there are then many fewer jobs albeit for the same wage. Those who retain such jobs then start belonging to a privileged group of “insiders” blessed with unchanged income. The rest become “outsiders” to the active labour market who find themselves unable to compete against the insiders by offering a lower wage for which they would be willing to work.

And so we have in Greece the unhappy situation of high numbers of unemployed, long durations in current jobs and low economic freedom. Reform policies of recent years have apparently failed to deconstruct the privileges of insiders who continue to inflict suffering on the outsiders.

Can monetary policy help against the insiders?

If Greece had its own currency, its central bank could have tried at the beginning of the crisis to create a high inflation rate (through an expansionary monetary policy). This would have lowered the real wages while still holding nominal wages rigidly fixed. The drop in employment would have been lower and the inflation would have made the return of outsiders to jobs easier as the lower real wages of insiders (i.e. the hourly cost to the employer) continued to fall. For a lower (real) price, employers would have wanted to purchase more work.

Inside a monetary union, however, this option of weakening the insiders’ position by means of an independent monetary policy is not open to the Greek government. It is true that the announcement last week by the European Central Bank that it would buy about €1.1 billion worth of sovereign and private debt could be interpreted as an attempt to weaken the position of insiders in Greece, Spain, France and Italy. After all, the goal of the ECB is to increase inflation back to around 2%. But even if the measure did manage to increase the inflation rate, it is very doubtful whether any significant real wage adjustments would follow. Paul Krugman estimates that the expected inflation rate over a five-year period has increased from 0.3% to 0.5% as a result of the programme. That will not be enough to reduce insiders’ real wages noticeably. Country-specific changes remain essential.

With or without the euro: No way forward without deep reform

The truth is, the underlying reasons for the Greek tragedy would not go away even after the country’s exit from the Euro and after a strong devaluation of a new Greek currency. Whether Greece leaves or stays, with or without further debt cancellation, drastic changes are necessary for a lasting improvement. Changes that would liberate the people from oppressive corruption and set it on course of economic freedom.

It is doubtful that such necessary changes will come about with Alexis Tsipras at the helm. But hope dies last.

(This article has been translated from the German original by Petr Barton.)